By Sean Sparkman

Pathfinders’ Wealth

Retirement planning has traditionally focused on a familiar set of concerns, including market volatility, inflation, healthcare costs, taxes, and the possibility of outliving your savings. While these risks still matter, another, less-familiar issue is rising to the top of the list for retirees and pre-retirees alike.

This risk is known as “policy risk,” and while it may sound a little dry and technical, it is a risk that many retirees are experiencing in a deeply personal way.

Policy risk refers to the uncertainty created by government actions or potential government actions, including changes to Social Security, Medicare, military actions, taxes, retirement account rules, tariffs, healthcare policy, and spending.

A recent report published by the Center for Retirement Research at Boston College examined how increased policy uncertainty is affecting retirement planning behavior among older Americans. Researchers found that many households are responding by delaying retirement, saving more defensively, and becoming increasingly cautious with spending and investing.

In other words, retirees are no longer planning solely around markets. Increasingly, they are planning around the policies of their state, local, and federal governments. That shift has begun to change both the financial and emotional landscape of retirement.

Policy risk feels more serious than ever.

Older Americans have always felt the pressure of political uncertainty to some extent. Elections come and go. Tax laws change. Markets react. The difference in 2026, though, is that many retirees feel as if the pace and scale of change has ramped up dramatically.

Several major retirement systems appear to be under pressure simultaneously. Social Security funding concerns have become less abstract as shortfalls seem more possible. Medicare premiums continue to go up, with no end in sight, as do other price increases such as price hikes related to tariffs and inflation. Retirees also worry more about the enormous federal debt and actions the Federal Reserve may take to reduce that debt. Also contributing to retirement system pressure are tax law changes, market volatility tied to policy decisions, and interest rate uncertainty.

For retirees living on fixed or semi-fixed income streams, even relatively modest policy changes may wind up having an outsized impact because retirees may not be able to work more or wait decades for markets to recover. Retirement is less forgiving because the margin for error is smaller. These realities explain why policy uncertainty is increasingly influencing retirement behavior, even before any actual policy changes occur.

Social Security anxiety is real.

Perhaps no issue creates more concern among retirees than Social Security. For millions of Americans, Social Security is not just a source of additional income, it is the pillar of their retirement plan.

According to federal projections, the Social Security Old-Age and Survivors Insurance Trust Fund could face depletion within the next decade if reforms are not enacted. While this does not mean Social Security is “going bankrupt,” it does mean policymakers will eventually need to address funding gaps through some combination of higher payroll taxes, increased retirement ages, “means testing,” reduced benefits, or modified benefit formulas. Uncertainty surrounding those possibilities creates anxiety long before any reforms actually happen.

Some workers nearing retirement are now wondering if they should claim benefits early since it is possible benefits could be reduced later. Some pre-retirees express concerns that taxes on Social Security are likely to increase. Many people within 10 years of retirement age are asking themselves “How dependable will Social Security really be 15 or 20 years from now? “

Ironically, fear about future changes can sometimes lead retirees to make emotionally driven choices that may reduce long-term financial security, such as claiming benefits too early or becoming overly conservative with investments.

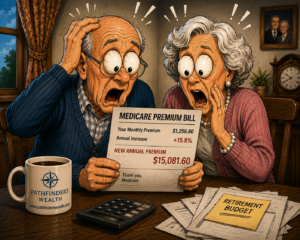

Medicare and health costs are more stressors.

Healthcare remains another major source of retirement stress, with many retirees surprised to discover that Medicare is far from free. Medicare premiums, deductibles, prescription costs, and supplemental coverage expenses continue rising steadily and can throw a retirement plan off balance.

Some higher-income retirees could face an additional challenge through IRMAA (Income-Related Monthly Adjustment Amount) surcharges, IRMAA is a surcharge added to Medicare Part B and Part D premiums for beneficiaries with higher incomes, based on a two-year lookback at tax returns. For example, in 2026, individuals with a 2024 MAGI over $109,000 or married couples over $218,000 will pay increased monthly premiums ranging from roughly $14 to $487 extra for Part B, creating a frustrating dynamic for retirees who save diligently and accumulate sizable retirement accounts.

These retirees may eventually trigger higher Medicare costs through RMDs (Required Minimum Distributions.) In other words, since required account withdrawals increase taxable income, some retirees will see net income shrink when they trigger Medicare surcharges through IRMAA. This situation seems like a hidden tax on responsible saving.

At the same time, healthcare inflation continues to outpace many retirees’ budgets. Even though overall inflation has moderated from recent peaks, older Americans are still facing rising costs for the goods and services they need most.

Many retirees discover that their personal inflation rate feels much higher than the official numbers suggest.

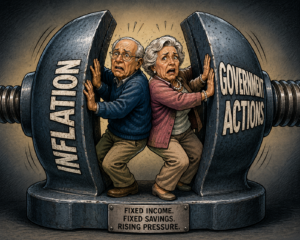

Inflation hurts worse for retirees.

Inflation affects everyone, but retirees often experience it more intensely because their spending patterns are concentrated in essentials. A younger worker may offset inflation through career advancement or wage increases, but most retirees don’t have that flexibility.

Inflation creates another layer of policy-related anxiety because it silently erodes purchasing power over time. Even so-called “modest” inflation compounds significantly over a 20- or 30-year retirement. For example, using a 3% annual inflation rate, a retiree needing $60,000 annually today would need more than $108,000 per year in roughly 20 years just to maintain the same purchasing power. This is why increasing numbers of retirees worry that fixed-income sources alone may not be enough.

Policy uncertainty can turbocharge market volatility and sequence risk.

Policy uncertainty is a significant contributor to market instability. Recently, we’ve seen firsthand how tariffs, tax policy, trade disputes, federal deficits, geopolitical tensions, and interest-rate decisions can all create sharp market swings.

For retirees, such volatility can be especially dangerous during what planners call the “retirement risk zone,” the time shortly before and after retirement when poor investment returns can permanently damage portfolio sustainability. Researchers refer to this type of risk as “sequence-of-returns risk.” When you experience sequence of returns risk, large losses early in retirement may force you to withdraw assets from declining portfolios. Doing so greatly reduces your ability to recover later. Sequence risk becomes even more stressful when you are unsure whether government policy itself is the cause of volatility.

Is retirement anxiety becoming a financial risk of its own?

One of the more overlooked consequences of policy uncertainty is the psychological impact.

Increasingly, retirees are not just worried about markets or inflation. They are worried about what comes next politically, economically, and institutionally. Uncertainty alone can alter retirement behavior in meaningful ways.

Recent retirement-confidence surveys show many Americans feel less secure about retirement today than they did just a few years ago, despite relatively strong market performance over certain periods. These surveys emphasize that it’s more than account balances alone that drives retirement anxiety today. The psychological impact is substantial and is causing some Americans to respond by deciding to delay retirement, postpone major purchases and life decisions, avoid long-term financial commitments, or shift toward cash.

These precautions may be wise in some cases, but it’s worth remembering that too much caution can also carry risk.

For instance, retirees who move entirely to cash out of fear may struggle to keep pace with inflation. Others may postpone retirement repeatedly, not because they are financially unable to retire, but because they no longer feel emotionally secure enough to make the transition.

Financial planners sometimes describe this as “retirement paralysis”, the inability to feel comfortable making major long-term decisions in an environment that feels unstable and constantly changing.

Ironically, fear of risk can itself become a retirement risk.

Some retirees under-spend unnecessarily and reduce their quality of life. Others abandon carefully designed investment plans after unsettling headlines or political conflict.

The emotional side of retirement planning is often underestimated, but it matters tremendously. Retirement is not just a math problem. It is also a confidence problem. A financial plan that looks perfect on paper but causes constant anxiety may not actually be sustainable for the person living it.

Even the wealthy feel uneasy.

Maybe it’s not so surprising to discover that even affluent retirees often feel financially insecure. Retirement experts are starting to see that a large number of households with substantial savings continue to worry about things such as long-term care expenses, taxes, market ups and downs, and policy changes.

At the same time, average retirement savings remain relatively modest for much of the population. That combination creates a troubling situation where retirees with limited savings feel vulnerable and those who’ve accumulated sizable savings still do not feel safe.

As I see it, this highlights an obvious truth: retirement confidence is not determined solely by wealth. Predictability matters too. When retirees feel like the rules keep changing, confidence declines, even when their portfolios remain relatively healthy.

What can you do about policy risk?

You can’t control DC policymakers, but you can control how prepared and adaptable you are. I encourage several strategies to help my clients reduce policy-related retirement stress.

One of these approaches is to develop multiple streams of retirement income. If you rely entirely on one source of income, you may be more vulnerable to future policy or market changes.

Diversifying retirement income may include maximizing Social Security, using dividend-paying investments, purchasing specific types of annuities, maximizing cash reserves, life insurance strategies, acquiring cash-flowing assets or businesses, or even taking on gig or other part-time work. The goal here is not necessarily to maximize returns but to instead create resilience.

Another way to offset policy risk is to focus on tax diversification. You might want to spread assets spread across taxable accounts such as tax-deferred accounts and Roth accounts.

Rigid withdrawal strategies can become dangerous during volatile periods. Flexibility in your spend-down approach, especially in discretionary spending, tends to improve the long-term sustainability of retirement assets. Even modest spending adjustments during challenging market environments may reduce pressure on portfolios significantly.

Likewise, liquidity is a critical factor, particularly during economic disruptions and policy uncertainty. You’ll want adequate emergency reserves to help keep from relying too heavily on credit or making panic-driven decisions you may later regret.

Cash reserves may not generate exciting returns, but they can provide a measure of emotional stability when you encounter uncertainty.

Other methods of decreasing retirement anxiety might include:

Delayed retirement (if practical) Incorporating a “phased” or delayed retirement could help you in many ways. You’ll increased your Social Security benefits, shorten the time that your savings must last, allow you to make additional contributions to accounts, and in some instances, preserve your health insurance options.

Finally, and I’d like to suggest that this may be the most important principle of all. You should resist the temptation to react emotionally to policy uncertainty. I know it can feel easier said than done. However, retirement portfolios built on a foundation of fear are rarely successful in the long run. Instead of jettisoning your long-term investment plans, rushing to claim Social Security earlier than needed, or moving to cash only, a better approach is the balanced one. Prepare wisely, diversify intelligently, retain your ability to pivot and reset as needed, and avoid panicking.

Sean’s Summary

Retirement planning is becoming more complicated because older Americans must now navigate both financial risk and policy risk simultaneously.

The uncertainty is real. But it does not automatically signal disaster.

The retirees who may fare best over the coming decade are probably not those chasing the highest returns, but those building adaptable, diversified, and flexible income strategies capable of weathering changing economic and political conditions.

In today’s environment, retirement security increasingly depends not just on what the markets do, but also on what policymakers do next. And perhaps most importantly, on whether retirees can remain calm and adaptable enough to avoid letting uncertainty itself become the greatest risk of all.

Sean R. Sparkman

Pathfinders Wealth

(248) 487-9148

www.pathfinderswealth.com

*As an Accredited Investment Fiduciary® I am legally obligated to prioritize my clients’ interests above

my own. I am committed to providing exceptional fiduciary care beyond that of other advisors. You can

send your questions or ask for an appointment by replying to this You can also call me at (248) 487-9148

during regular business hours.