*This article and video are provided for educational and informational purposes only and should not be interpreted as a recommendation, solicitation, or endorsement of any particular investment strategy, security, or financial product. The material presented is not intended to provide investment, legal, or tax advice. Individual financial circumstances vary, and readers should consult with a qualified financial advisor or tax professional before making any investment decisions.

by Sean Sparkman

Pathfinders Wealth

As investors reach their mid-50s and beyond, portfolio construction becomes slightly more complex and nuanced. The focus shifts from merely accumulating assets to managing taxes, improving overall portfolio efficiency, and enhancing returns without unnecessary risk.

Two strategies attracting growing attention among more sophisticated investors are direct indexing and the 130/30 long-short equity strategy. While they operate differently, both aim to address the limitations of traditional index investing by providing portfolio managers greater flexibility. For retirees and those approaching retirement, understanding these two approaches can help broaden the set of tools available for building and managing a portfolio.

The Limits of Traditional Index Investing

Traditional index funds have earned their popularity for good reason. They provide:

- Broad diversification

- Low costs

- Transparent exposure to the overall market

However, index funds also have limitations. Investors who buy an index fund accept the index as is, even if some companies seem overvalued, poorly positioned, or misaligned with their broader goals. Investors in index funds also lack control over their taxes. Gains and losses occur at the fund level, and the investor receives the distributions. Direct indexing and long-short equity seek to address these constraints in different ways.

Direct Indexing: Owning the Index One Stock at a Time

Direct indexing replicates a market index’s performance by owning its individual securities rather than purchasing an index fund. Investors hold each index stock in proportion to its weight. This creates a customized version. Advances in technology and portfolio management systems have made direct indexing increasingly accessible to individual investors. While your main is still to track a benchmark index, direct indexing offers some particular advantages.

Direct indexing can provide greater tax efficiency

Because the investor owns individual stocks, losses can be harvested precisely. If a company declines in value, that position can be sold to realize a loss, with proceeds used to buy a similar holding and maintain market exposure. For retirees managing taxable portfolios, this process can help offset gains elsewhere and potentially reduce the tax burden over time.

Direct indexing allows for customization

Direct indexing also allows investors to tailor the portfolio to their preferences. For example, investors may choose to:

- Exclude certain companies or industries.

- Tilt toward dividend-oriented stocks.

- Adjust sector exposure based on personal convictions.

Such customization is not possible in a single index fund.

More precise portfolio management

Direct indexing allows portfolio manager to make targeted adjustments without accepting every index component, while still maintaining broad market exposure.

For investors who value tax efficiency and personalization, direct indexing can represent a meaningful improvement of the indexing concept.

Introducing the 130/30 Long-Short Strategy

Another way to increase portfolio flexibility is the “130/30 long-short equity approach. Most traditional equity portfolios are long-only: managers buy stocks they expect to perform well and sell or reduce holdings they dislike. They cannot profit from stocks expected to decline, as ‘long’ means owning stocks. ‘Short’ means selling borrowed stocks, which long-only strategies do not permit. This limitation can restrict how effectively a manager can express their investment views.

The 130/30 approach addresses this constraint by allowing both long positions, meaning that an investor owns stocks expected to rise, and short positions where you are selling borrowed stocks expected to fall, within the same portfolio.

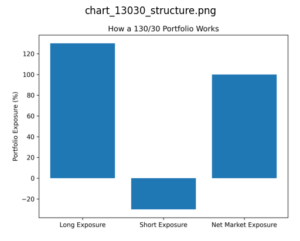

How does a 130/30 portfolio work?

The numbers reflect the portfolio’s structure.

- 130% of the portfolio is invested in long positions—stocks expected to outperform.

- 30% is invested in short positions—stocks expected to under-perform.

The portfolio maintains 100% net equity market exposure despite these positions.

Here is a simplified example.

Consider an investor with $100,000. The manager buys $100,000 in favored stocks, shorts $30,000 in expected underperformers, and uses those proceeds to buy another $30,000 in favored stocks.

The result is:

- $130,000 in long positions

- $30,000 in short positions

- $100,000 in net market exposure

Chart: Structure of a 130/30 portfolio

This chart illustrates the basic mechanics of a 130/30 strategy. The portfolio holds 130% of its capital in long positions while simultaneously maintaining 30% in short positions. Because the proceeds from the short positions are reinvested in additional long holdings, the net exposure to the market remains 100%. This allows the portfolio to maintain market-like behavior while giving the manager additional flexibility to express investment insights. Because the portfolio’s overall exposure to the market remains similar to a traditional equity portfolio, these strategies are often referred to as “beta-one” strategies. The goal is to maintain the same overall market sensitivity as the benchmark while generating additional return—known as alpha—through stock selection.

On the other hand, a passive index fund also has a market beta near 1.0 but, by definition, an expected alpha of zero.

Why the Ability to Short Can Matter

During the research process, portfolio managers typically identify not only companies they expect to perform well, but also those they believe may struggle. In a long-only strategy, managers can overweight their best ideas, but negative views are limited to avoidance. Short selling allows the manager to go further.

During the research process, portfolio managers typically identify not only companies they expect to perform well, but also those they believe may struggle. In a long-only strategy, managers can overweight their best ideas, but negative views are limited to avoidance. Short selling allows the manager to go further.

Short selling involves borrowing shares of a security and selling them with the goal of repurchasing them later at a lower price. If the stock declines, the difference between the selling price and the repurchase price represents profit. If the price rises, the short seller incurs a loss. By incorporating short positions, a portfolio manager could potentially benefit from both rising and falling markets.

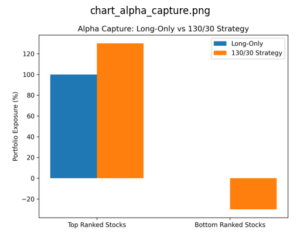

Chart: Alpha capture in long-only versus 130/30 portfolios

Traditional long-only portfolios can only express positive investment views by over-weighting stocks expected to outperform. When a manager identifies companies expected to underperform, the only option is to avoid them. A 130/30 strategy allows the manager to take short positions in those weaker companies, potentially capturing value from both sides of the stock selection process. This expanded opportunity set is one of the primary reasons institutional investors began exploring long-short extension strategies.

Long-only portfolios express positive views by overweighting strong stocks. To act on negative views, managers can only avoid weak companies. The 130/30 strategy allows shorting weaker companies, capturing value from both sides. This broader opportunity set attracts institutional investors to long-short strategies.

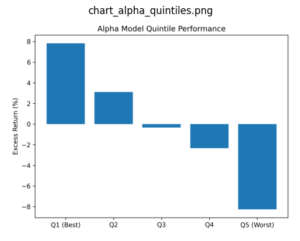

Chart: Performance of top versus bottom-ranked stocks

Quantitative research frequently finds that top-ranked stocks tend to outperform, while lowest-ranked stocks tend to underperform. A long-only strategy cannot profit directly from the weakest stocks, but a 130/30 strategy allows managers to short them, potentially enhancing overall returns.

Understanding the Risks of Short Selling

While short selling introduces new opportunities, it also brings additional risks. When an investor purchases a stock (a long position), the maximum loss is limited to the amount invested. A stock cannot fall below zero, so the most an investor can lose is the initial investment. Short selling works differently. In theory, a stock’s price can continue rising with no limit. That means the potential loss on a short position (betting the price will fall) is not capped and could, in extreme cases, exceed the amount originally invested.

Other considerations include:

• Stocks must be borrowed to sell short.

• Borrowing costs vary with supply and demand.

• Illiquid securities may be hard to borrow.

• Lenders may recall shares, forcing inconvenient closures.

• Stocks must be borrowed to sell short.

• Borrowing costs vary with supply and demand.

• Illiquid securities may be hard to borrow.

• Lenders may recall shares, forcing inconvenient closures.

These factors make implementation skills and risk management particularly important.

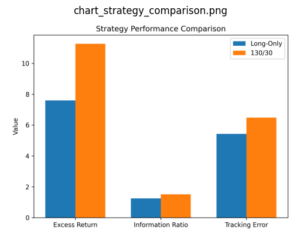

Chart: Return and risk characteristics of long-only versus 130/30 strategies

A diversified portfolio of short positions can reduce some short-selling risks. When combined with long positions in a 130/30 structure, overall market risk may be reduced.

In essence, long and short positions can partially offset one another, allowing the portfolio to focus more on stock selection than on broad market movements. Research comparing the two approaches finds 130/30 portfolios may offer higher excess returns with only slightly more risk. Measures like tracking error and information ratio show returns improve more than volatility rises.

Long-Short Strategies

Interest in long-short strategies grew in the early 2000s, after the tech bubble downturn. Institutional investors sought new returns beyond long-only portfolios.

During that period, the investment industry saw rapid growth in alternative strategies, including hedge funds, portable alpha strategies, and private equity. Long-short extension portfolios, including variations such as 120/20 or 140/40, emerged from this wave of innovation. The foundation for these strategies goes back further. Modern portfolio theory and academic research indicate that allowing both long and short positions can improve efficiency and flexibility.

During that period, the investment industry saw rapid growth in alternative strategies, including hedge funds, portable alpha strategies, and private equity. Long-short extension portfolios, including variations such as 120/20 or 140/40, emerged from this wave of innovation. The foundation for these strategies goes back further. Modern portfolio theory and academic research indicate that allowing both long and short positions can improve efficiency and flexibility.

Where These Strategies May Fit in Retirement

For retirees and those approaching retirement, the goal is often not simply to maximize returns but to improve portfolio efficiency.

For retirees and those approaching retirement, the goal is often not simply to maximize returns but to improve portfolio efficiency.

Direct indexing can be especially appealing for investors who:

• Hold sizable taxable portfolios

• Want greater control over tax outcomes

• Value customization and flexibility

Meanwhile, 130/30 strategies may appeal to investors who:

• Want active equity exposure

• Believe skilled managers can identify both winners and losers

• Are comfortable with more complex portfolio structures

• Hold sizable taxable portfolios

• Want greater control over tax outcomes

• Value customization and flexibility

Meanwhile, 130/30 strategies may appeal to investors who:

• Want active equity exposure

• Believe skilled managers can identify both winners and losers

• Are comfortable with more complex portfolio structures

Should we expand the conversation around portfolio design?

Retirement investing today often extends well beyond the traditional mix of stocks, bonds, and mutual funds. Advances in technology and financial research have created new ways to structure portfolios and manage risk. Direct indexing and 130/30 strategies represent two examples of how portfolio construction continues to evolve. While neither approach is appropriate for every investor, both illustrate how modern investment strategies can offer greater flexibility, improved tax management, and potentially more efficient use of investment insights.

For investors preparing for retirement—or already living in it—understanding these strategies can inform conversations with financial professionals and expand the range of tools available to manage long-term wealth.

For investors preparing for retirement—or already living in it—understanding these strategies can inform conversations with financial professionals and expand the range of tools available to manage long-term wealth.

*This article draws on research and data presented in “An Empirical Analysis of 130/30 Strategies: Domestic and International 130/30 Strategies Add Value Over Long-Only Strategies” by Gordon Johnson, Shannon Ericson, and Vikram Srimurthy, published in The Journal of Alternative Investments. Their work examines the historical performance and portfolio characteristics of 130/30 strategies relative to traditional long-only equity portfolios.

If deeper analysis and data are your thing, you can download the Wharton analysis paper here:

Because the portfolio’s overall market exposure remains similar to that of a traditional equity portfolio, these strategies are often referred to as “beta-one” strategies. The goal is to maintain the same overall market sensitivity as the benchmark while generating additional return—known as alpha—through stock selection.

By contrast, a passive index fund also has a market beta near 1.0 but, by definition, an expected alpha of zero.

At Pathfinders Wealth, we strive to help our clients discover the very best portfolio strategies based on their risk tolerances, goals, and relationships with money. For many, newer strategies such as 130/30 and direct indexing may be worth researching and implementing. If you are interested in discovering more about how your portfolio can become more flexible, tax-efficient, and mitigate against risk, call our office for a complimentary portfolio review.