By Jerry Yu

“The Family Money Doctor”

Working people in the United States face a significant and growing retirement savings gap. By some estimates, over 57 million US-based workers cannot access an employer-based retirement plan.

Several states have implemented what are known as Automatic Individual Retirement Account (AUTO-IRA) programs to resolve this issue. The goal of these programs is for more people to save more for retirement. While this concept has some merit, there are also certain limitations to research if you’re considering joining your state’s program.

For most Americans, staying optimistic about retirement is getting harder and harder.

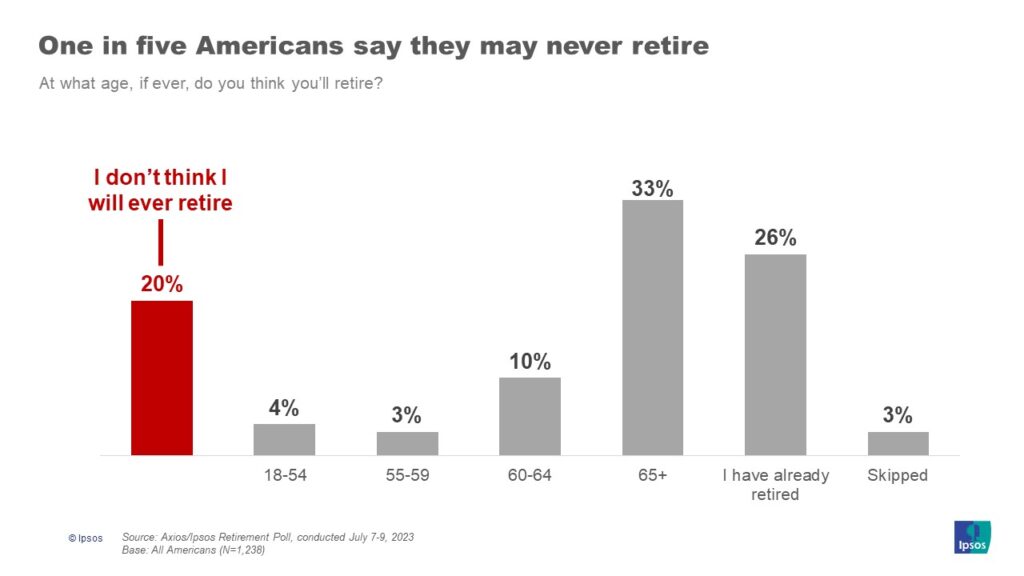

Research leader Axios/Ipsos recently polled some retirees and pre-retirees to determine how American attitudes toward retirement have shifted. The polls indicated that:

Nearly one in five US seniors believe that they will never retire. Of those, over 70% say they feel they won’t have enough money to fund their retirements. 40% of those over 55 polled also stated that even if they manage to retire, they aren’t sure if it will be at the anticipated time.

Given our current economic challenges, it’s easy to understand why thoughts about retirement are trending negative, especially when you know that not having access to an employer-sponsored retirement plan is partly to blame.

The chart below shows that most pre-retirees are not saving enough money to produce adequate income streams when they retire. Utilizing data from Vanguard’s 2022 “How America Saves 2022” report, the chart illustrates that accessible retirement savings options are necessary for all age groups to correct the gap problem.

Chart: 401(K) Balances by Age

The table below illustrates the average and median 401(k) balances of individuals in the United States, categorized by age groups. These figures offer valuable insights into the retirement savings landscape in the country.

Age Bracket Median 401(k) Balance Average 401(k) Balance

< 25 $1,786 $6,264

25 – 34 $14,068 $37,211

35 – 44 $36,117 $97,020

45 – 54 $61,530 $179,200

55 – 64 $89,716 $256,244

65+ $87,725 $279,997

Table Source: Gabriel Cortes / CNBC

Could state-run retirement programs be a solution?

So far, 19 states have passed laws to create “work and save” programs. These are attempts to make it easier for people whose employers do not offer retirement plans to save. Several of these plans are already in place and running, with others due to come on board later this year and 2024.

Most state plans involve what’s called an “Auto IRA.” The state-run programs mandate most private employers without their own savings plans to enroll their employees in the state option at a pre-determined savings rate. Typically, this rate is anywhere from 3 percent to five percent of a person’s wages. This amount is automatically deducted from paychecks and increases annually unless a person opts out.

While every state’s automated plan parameters are different, some features are similar. For instance, in most state-run savings plans, contributions are directed into Roth IRAs. The Auto-IRAs are managed by private financial companies but overseen by state-appointed boards. Since Roth contributions come from after-tax money, withdrawals in retirement are tax-free.

State plans also offer multiple investing options, including target-date funds, or TDFs, that customize the investment mix to an individual’s projected retirement date. As is the case with employer-sponsored plans, most state-run savings solutions also offer various stock, bond, and income funds. Enrolled employees must also pay administrative fees, just as they would with an employer-provided qualified plan.

Some states encourage smaller companies and non-profits to voluntarily offer workplace savings plans through state-run marketplaces or multiple employer plans. (MEPs)

State–run programs have pros AND cons.

Thus far, state-initiated savings programs have assisted people in saving over $840 million. This uptick is an encouraging start, to be sure. Proponents claim numerous worthwhile advantages to having the state manage retirement plans. Some benefits include:

- Auto-IRAs and other state programs bridge the retirement gap by allowing nearly everyone who works to have a qualified retirement plan.

- The automatic enrollment feature of Auto IRAs creates a “set and forget” approach that lets employees save without participating actively. Employees are enrolled by default but can opt out if they desire. Default enrollment and automatic payroll deductions are critical in overcoming psychological barriers that may keep people from saving. Contributions are taken before that cash burns a hole in an employee’s pocket.

- Most state-run plans have lower fees and administrative costs when compared to traditional company plans.

- Federal regulations such as the 2019 Secure Act bolster state plans. Such Federal legislation encourages more small businesses to offer retirement plans. By joining pooled employer plans such as MEPS, they experience fewer administrative burdens, and associated costs tend to decrease.

State–run savings plans have some cons, too.

- They lack a “matching” feature. Most Auto-IRA plans, unlike employer plans, do not offer any matching contributions. The matching aspect is one reason employees might choose one company over another when looking for a new employment opportunity.

- The contribution limits are lower.

High-income earners wanting to play catch-up or save more aggressively might not like that Auto-IRAs have lower contribution limits than 401k plans.

- State plans are generally not as flexible and customizable as 401ks. Many employers don’t use state programs because they find them too restrictive or lacking quality investment options.

Mandatory enrollment may be off-putting to some employers. Previously, I mentioned that automatic enrollment of employees can be a good thing. However, some employers push back against mandatory automatic enrollment because they say it leads to contributions without an employee’s active consent.

Yu’s Views:

State-administered AUTO-IRA plans are making significant progress in addressing the retirement savings gap crisis in the United States by giving Americans more access to savings accounts. These programs may become valuable in ensuring more Americans save enough money to fund their retirements. However, auto-IRAs may have crucial limitations, such as lower contribution limits and lack of employer matching.

Ultimately, the future of auto-401k plans depends on their ability to incentivize employers and employees to participate more actively in securing their financial futures.

If you’re considering joining a state retirement savings plan, I will gladly give you my qualified second opinion and show you some alternative strategies. Contact me via one of the ways listed below. I’m here to help!

Contact me here:

https://www.reignfinancialservices.us/our-process

Or:

Irvine Office

Phone: (626) 890-0090