By Sean Sparkman

Until recently, inflation was something many Americans rarely thought much about. For the

most part, prices tended to move gradually. Fuel costs were relatively manageable, and retirees

had more predictable costs around which they could build their financial plans.

Then, the world experienced an epic inflation shock in the early 2020s. All of a sudden,

groceries cost dramatically more, insurance premiums jumped, and eating out became a luxury.

Even essential utilities became noticeably more expensive. And, while inflation has cooled

from its peak, many retirees and near-retirees are accepting the uncomfortable truth that when it

comes to prices, what goes up rarely comes back down.When you are living on a fixed or semi-fixed income, inflation can quietly become one of the

greatest threats to your long-term retirement security.

According to research from the Center for Retirement Research at Boston College (CRR),

inflation harms retirees more than near-retirees because retirees often have less income tied to

rising wages and may rely more heavily on fixed-income sources.

In 2024, a report prepared for Congress by the U.S. Department of Labor noted that inflation can

significantly reduce purchasing power over time and complicate retirement planning decisions.

The problem is not just that the cost of living rises. The real issue is compounding.

For instance, a retiree who needs $60,000 annual income in 2026 is likely to require far more

than that 15 or 20 years from now just to maintain the same lifestyle.

Inflation reduces purchasing power for all of us. Your dollars buy less and less every year.

Although that may not sound catastrophic, the compounding effect kicks in and your finances

take a hit. When you are no longer working, the impact can be dramatic.

A retiree spending $5,000 per month today could easily need $6,700 per month in 10 years at 3%

inflation. In 20 years, that could increase to over $9,000 per month in 20 years.30 years into

retirement you might require $12,000 per month to finance your current lifestyle. That is the

danger of compounded inflation.

Working people sometimes offset inflation through raises, promotions, side income, or career

changes. Retirees typically do not have that flexibility. They often retire on Social Security,

pension income, withdrawals from investment accounts, bond interest, or annuity payments.

While some of these income sources adjust for inflation, others do not.

Worst still, official inflation numbers are computed in ways that often do not reflect the expenses

retirees actually experience. Older Americans tend have expenditures in categories that have

seen persistent, unrelenting inflation pressure. Costs for healthcare, prescription medications,

insurance, utilities, housing and home maintenance, food, and property taxes continue to

increase, adding additional elements of unpredictability to retirement income planning.

Recent reports suggest retirees may experience “personal inflation” rates much higher than

headline CPI figures because their spending patterns differ from younger households.

For example, a younger worker may absorb inflation by delaying vacations or eating out less

often. A retiree facing rising medication costs or Medicare premiums may have fewer choices.

Healthcare inflation alone can dramatically reshape retirement budgets over time.

Those approaching retirement face a unique challenge when it comes to dealing with inflation.

High inflation often leads to higher interest rates, a situation that may pressure both stock and

bond markets simultaneously. That creates a dangerous sequence for someone within five years

of retirement. Pre-retirees might discover their portfolios declining due to market volatility, with

inflation increasing future income needs. They may also see that bonds are not providing the

same level of stability they once did and they don’t have a long enough timeline to recover from

losses. As I have mentioned in previous articles, inflationary pressure can force retirees into

making less-than-ideal revisions to their retirement plans such as delaying retirement, working a

part-time job, taking on more risk, or reducing their legacy goals.

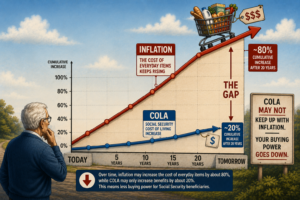

Social Security COLA might help…a little

One major protection against inflation retirees have is the Social Security Cost-of-Living

Adjustment (COLA). Since 1975, Social Security benefits have generally received annual

inflation adjustments tied to the Consumer Price Index.

COLA can help preserve some of your purchasing power, with several important caveats.

Many retirees argue that their actual costs rise faster than COLA increases.

Medicare premiums frequently rise alongside COLAs, reducing some of the increase.

Recent projections suggest Medicare costs may continue climbing substantially in

coming years

Social Security was never designed to replace full working income for most Americans.

It was intended to supplement savings and other retirement resources. If a household is

heavily dependent on Social Security, inflation can still create financial strain despite

annual adjustments.

Inflation often complicates withdrawal strategies as well. The well-known “4% rule” used by

many planners assumes retirees will increase withdrawals over time to keep pace with inflation.

However, when inflation spikes unexpectedly, retirees may find themselves withdrawing

substantially more than the anticipated 4% just keep their retirement afloat.

If retirees experience market declines, higher withdrawals, and elevated inflation all at once,

their portfolios will deteriorate much faster than expected.

This is one reason many retirees are increasingly interested in guaranteed income sources that

may reduce dependence on volatile portfolio withdrawals.

How can you manage inflation risk?

I will be the first to admit that there is no perfect inflation-proof retirement plan. But,

Pathfinders Wealth does have many proven approaches to help our clients improve their

portfolio resilience.

1. We encourage our clients to maintain some growth strategies

As you can imagine, completely abandoning growth investments may result in long-term

inflation risk. Even more conservative retirees often benefit from maintaining diversified

exposure to equities or other growth-oriented assets.

2. We help you build multiple streams of income.

Relying on only one source of retirement income is a sure fire way to increase vulnerability. By

combining Social Security with other sources of income such as investment withdrawals,

dividend income, part-time work, whole life cash value, cash-flowing businesses and other

diversified income, you increase your flexibility and resilience.

3. Some people might want to delay Social Security to increase income.

Delaying Social Security benefits can permanently increase monthly income, creating a larger

inflation-adjusted lifetime income stream.

4. We can help you create and maintain an emergency fund.

Inflation can cause unexpected spikes in spending. By maintaining liquid reserves you might be

able to avoid selling assets during unfavorable market conditions.

5. Together, we will re-evaluate spending assumptions.

Many retirement plans still assume relatively low inflation. At Pathfinders, we partner with our clients to help them understand and re-think their previous spending assumptions. Today’s aggressive inflationary environment may challenge more conservative assumptions, especially concerning inflation and its impact on healthcare, taxes, long-term care, and housing. You should consider stress-testing retirement plans using higher inflation scenarios to help identify weaknesses before they become crises.

Sean’s Summary

For decades, retirement planning discussions focused heavily on market returns. Today, inflation

has re-emerged as a central concern for retirees and those about to retire.

Unlike market declines, inflation often feels relentless because it affects nearly every aspect of

daily life simultaneously. Your food costs rise, insurance, property tax, and utility bills go up,

seemingly all at once. The cumulative effect of these increases can quietly erode retirement

security even during periods when investment portfolios seem stable.

For this reason, Pathfinders Wealth focuses not just on building wealth, but on preserving your

purchasing power and increasing your adaptability and resilience. We know that in retirement,

it is not just about how much money you have. it is about what that money can still buy 10, 20,

or 30 years from now.

If you’d like to have us evaluate your current portfolio at no cost, contact my team today.

Sean Sparkman

Pathfinders Wealth (248) 487-9148