By George Politarhos

The Thrift Savings Program (TSP) was initially designed to give active and retired federal personnel a simple, cost-effective 401-k type plan. The TSP has worked exceptionally well, perhaps even better than anticipated. Many retired feds have achieved self-made millionaire status because of their Thrift Savings Plan. Also, the TSP boasts some of the lowest administrative fees in the business, allowing participants to keep more of their earnings.

The TSP breaks costs into two categories: investment and gross administrative expenses. Gross administrative expenses include things such as participant services, the printing of statements, notices, and publications, and recordkeeping. Gross administrative expenses are funded by forfeitures and fees, leaving net administrative expenses paid for by small reductions in fund earnings.

Investment expenses, namely fees paid to fund managers, are also financed by reductions in earnings. Each participant in a TSP fund pays the same percentage of their investment in the fund to offset expenses. This percentage is called an expense ratio, calculated by dividing costs by the fund’s average dollar amount.

Nearly every investment vehicle sold today charges a fee to help pay expenses. That’s why it’s critical to factor in such charges when making investment decisions, even if you are not using the MFW.

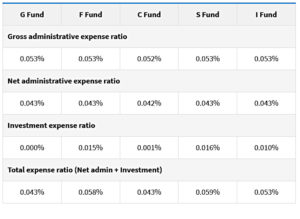

When you review the table below, you’ll notice the expense ratio for the F Fund was 0.058% in 2021. In other words, every $1,000 invested in the F Fund was reduced by 58 cents. It cost a participant investing $1,000 in the fund 58 cents for expenses, while a participant with $200,00 invested paid $116.00. Everyone pays the identical percentage, but the larger your investment, the more expenses you’ll pay. If you want to convert the table’s expense ratios to cost-per-$1,000 invested, move the decimal point one space to the right. For example, 0.042% becomes $0.42, or 42 cents. Table 1 also shows the gross administrative expense ratio, the net administrative expense ratio, and the investment expense ratio. By adding the net administrative expense ratio to the investment expense ratio, you get the final expense ratio, which measures how much expenses reduce a fund’s earnings

Source: TABLE 1 TSP.GOV

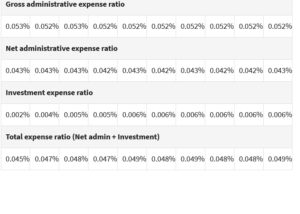

Table 2 gives you the same metrics for each Lifecycle (L) fund, comprised of various amounts of G, F, C, S, and I Funds. L Funds do not have separate expenses, so the expense ratios reflect the expenses of each underlying fund in the L Fund.

Table 2

However, changing market conditions, social investing considerations, and the desire for higher earnings than those of the C, S, F, or G funds have prompted significant upgrades to the Thrift Savings Plan. This recent overhaul now gives federal employees 5,000 new fund choices.

These improvements carry a price tag in the form of higher fees. TSP investors using the Mutual Fund Window (MFW) must absorb the MFW’s costs. That means a TSP participant wanting to invest in the MFW pays additional fees.

As of 2022, those fees are

- A $55 annual administrative fee

- A $95 yearly maintenance fee

- A per-trade of $28.75

- Other fees and expenses charged by each fund selected

Sorry about all the math, but there’s a method to my madness. As a Federal employee, you must be sure to consider the impact of fees and expenses on your retirement income. Accounting for costs applies to your TSP plan and all the other assets in your portfolio.

At first glance, fees may seem insignificant. But they tend to add up quickly, eating away any gains you might have. It’s a great idea to have a qualified federal benefits advisor review your portfolio and help you anticipate the impact of fees and expenses on your retirement and perhaps find ways to lower those expenses. If you’d like help determining the effect of costs and fees on your overall retirement plan, reach out to me, and I’ll be happy to assist you.