Created By The Macro Butler Via Zerohedge.com

by The Macro Butler via ZeroHedge

Contributed by Sean Sparkman, Pathfinders Wealth

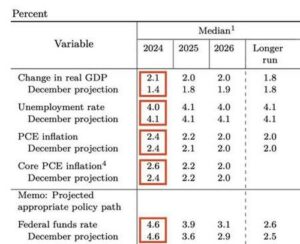

The key takeaways from the FED’s SEP are that it raised expected real GDP growth to +2.1%, lowered expected unemployment rate to 4.0%, kept expected PCE inflation at 2.4%, and raised expected core PCE inflation to 2.6%.

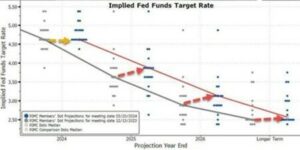

The FOMC, while indicating higher dots, was overshadowed by a politically dovish Powell, adding forward confusion regarding what the FED will actually be able to do in 2024 as the US moves into the inflationary bust phase of the business cycle.

While the consensus still expects three rate cuts for the year, starting in June, as inflation reaccelerates by the summer, the politically correct FED will, at best, be able to keep interest rates unchanged for the year as stagflation emerges by the summer. Would it not be politically driven, it should raise interest rates to combat the incoming Bidenomics-driven stagflation.

In the meantime, the consensus is still chasing the infamous pivot even Wall Street has been wrong for almost 2 years on that matter.

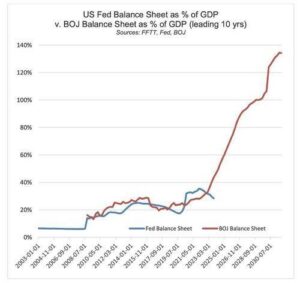

Nearly a year ago, the Congressional Budget Office (CBO) reported a $422B Federal budget deficit for Q1 2023. Fast forward to January 2024, the CBO announces a $509B deficit for Q1 2024. Revenue increased by 8%, but expenses rose by 12%, indicating a concerning trend. The US is now facing an evident debt spiral, with a deficit to GDP ratio nearing 8%, reminiscent of crises like the 2008 GFC and the 2020 pandemic. Some argue deficits don’t matter, citing Japan’s situation, but the US differs with twin deficits and a negative Net International Investment Position, making its debt outlook more precarious.

Unless the US drastically reduces entitlement and defense spending by 40%, which is improbable in an election year and amid widespread military tensions, such austerity measures are as unlikely as finding honesty in Congress. Without these essential cuts and transparent budgeting, policymakers will likely ignore another year of multi-trillion-dollar deficits, burdening current and future generations while resorting to inflation to mitigate debt by injecting more devalued currency into circulation.

While Developed Markets struggle with Fiscal Dominance, Emerging Markets debt presents winners in the form of government bonds offering high real yields supported by robust fiscal policies. As a result, central banks in EM are not only buying gold but also investing in EM local currency government bonds to utilize the earnings in EM currencies from intra-EM trade, which is gradually shifting away from the dollar. Most EM countries boast low debt, independent central banks offering high real rates, and sound economic structures. Additionally, EM countries do not impose sanctions on each other’s savings, rendering their bonds relatively safe. Recognizing these appealing attributes of EM bonds, other central banks are also allocating EM local currency bonds to their balance sheets, similar to their gold holdings.

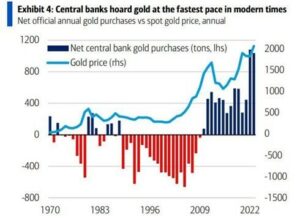

Simultaneously, as the USD has been weaponized amid the conflict between Ukraine and Russia, central banks around the world, particularly in Emerging Markets, have been accumulating gold at the fastest pace in modern history.

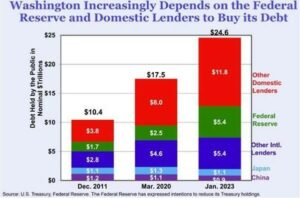

With the shift in US Treasury buyers from yield-insensitive entities like sovereign wealth funds and central banks to yield-sensitive buyers such as US households, pensions, and insurance companies, the Treasury may struggle to attract buyers for its bonds. Hypothetical rate cuts could lead to reduced demand from yield-sensitive buyers, potentially resulting in a steeper yield curve.

Despite the US unemployment rate nearing historic lows and interest rates remaining higher for longer than expected, consumer spending remains excessive, and credit card delinquencies are on the rise. This trend signals impending trouble and suggests that the precarious foundation of the US consumer economy may be on the verge of collapse.

Consumers are not the only ones defaulting on their debts; corporate bond defaults surged massively in 2023, especially for high-risk junk bonds, and the trend is continuing at a pace not seen since the 2008 GFC in 2024. Debts that were financed in a low-interest rate environment are due to mature in the next few years, amounting to over $1.8 trillion by 2028, according to the FED. When those payments come due, more companies will succumb to the default wave. If the junk bond market plunges, it could burst the broader $13.7 trillion corporate bond bubble and drag down the rest of the economy with it.

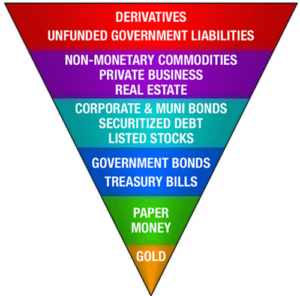

In that context, investors will have soon to reassess their investments through the lens of counterparty risk. John Exter’s Inverted Pyramid of Risk, introduced in the 1970s, offers insight into America’s vulnerabilities, particularly amidst an impending credit crisis centred around the USD. The pyramid organizes assets from highest to lowest risk, highlighting the interconnectedness where the removal of lower-risk assets can lead to a collapse of higher-risk ones, akin to a Jenga tower.

This risk hierarchy starts at the top with derivatives and unfunded government liabilities, which any form of financial turbulence can not only wipe out a participant’s initial investment but also entail additional losses. Warren Buffett notably dubbed them ‘financial weapons of mass destruction.’ Private Business Equity, Real Estate, and Non-Monetary Commodities include genuinely productive assets and commodities for economic growth but given their relation to the credit markets they prove highly sensitive during a deflationary recession, as exemplified by the 2008 financial crisis. Blue Chip Stocks, Corporate Bonds, and Sovereign Government Bonds are more conservative assets, appealing to long-term investors seeking yield beyond money market accounts and T-Bills. However, these assets are not immune to interest rate risks associated with FED policy and are still susceptible to substantial losses during recession/depression. Federal Reserve Notes & Treasury Bills sought for stability, are technically the first layer of what many call “risk-free” assets found in Federal Reserve notes and Treasuries. Even if one accepts this “risk-free” title (we do not), the solvency of the institutions holding these assets becomes a concern. At the foundational base of the pyramid, physical gold stands as the only asset devoid of counterparty risks or credit risks. Aligned with the foundational principles of what money should be, gold’s immutability and resistance to defaults, bankruptcy, devaluation, or a plunge to zero make it unique as the last stand in financial collapse.

This model also unveils the flow of capital during economic phases.

During credit expansions, capital moves up the inverted pyramid toward higher-risk, lower-liquidity assets, reflecting investors’ willingness to take on greater risks for higher returns. As the pyramid broadens, capital is reused as collateral multiple times, amplifying theoretical contracted capital on higher layers, such as the derivative layer. In a crisis, capital is moving down the pyramid towards lower-risk assets like bonds, cash, and gold, illustrating a return to stability. The insight from John Exter’s pyramid underscores the unseen layers of risk in financial flows, urging a broader consideration beyond balance sheets in investment decisions. Amidst flaws in the financial system, gold offers liberation from credit and government risks and currency devaluation. As sovereign debt defaults loom and liquidity expansion slows, markets will face short-term risks to liquidity-sensitive assets in 2024.

Read more and discover how to position your portfolio here:

https://themacrobutler.substack.com/p/a-house-of-cards-on-borrowed-times

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.

Ready for a different approach to wealth and retirement planning?

Are you concerned you:

- Might outlive your savings in retirement?

- Will start Social Security at the wrong time?

- Could fail to account for potentially expensive healthcare costs?

- Are missing out on higher interest rates?

- Will enter retirement with too much debt?

- Could have an imbalance in your portfolio?

If so, then you should consider reaching out to a retirement income planner knowledgeable in helping those newly-retired or within five years of retirement get the most from every dollar of their savings.

A fiduciary investment advisor, Michigan-based retirement income specialist Sean Sparkman focuses on guiding clients in creating the streams of retirement income they’ll need to see them through during an unpredictable economic cycle. Despite current market volatility and a challenging low interest rate environment, Sean says you still have options you can put in place right now to ensure that you do not run out of income. Choosing such opinions will go a long way toward keeping your wealth protected from future market downturns and provide you with safer, saner growth opportunities.

While most financial advisors are more than happy to provide you with investment tips and growth opportunities for your portfolio, few of them specialized training necessary to take what you’ve saved and convert it into streams of long-term, sustainable income. Sean Sparkman has devoted much of his time and energy to gaining the specific skills and product knowledge to help his clients during the spend-down phases of their financial lives. Retirees who work with Sean praise his hands-on approach, his patience, and ability to answer even their most complicated questions. Many of Sean’s clients claim they are able to spend their savings with greater confidence and less stress.

Sean Sparkman addresses the needs of seniors about to leave their jobs or who are recently retired, across the United States. As a full-service financial services provider, Sean has the tools, skill sets, and products needed to handle most any retirement planning situation. He can meet digitally or in person with seniors looking for more flexibility, control, liquidity, and safety for their wealth.

See what Sean’s clients have to say about buying #financialservices and products online and about their experiences working with Sean. Check out the videos below.

Office Line: (313) 246-9278

Cell Phone: (248) 325-7059

Safe Money Trends Articles: www.safemoneytrends.com/author/seansparkman/

Learning Center: seansparkman.retirevo.com

Company Site: safeandsoundretirement.net

Insight Folios: www.insightfolios.com/team-member/sean-sparkman

Facebook: facebook.com/safesoundretirement

Instagram: instagram.com/seanrsparkman